Soma Mater Newsletter – 27.04.2026

Welcome to the SOMA MATER weekly newsletter.

At SOMA MATER, we deliver comprehensive research and advisory services focused on Food & Water Security and Net Zero Transition in the MENA Region. To help our clients navigate these topics and understand the regional narrative, we accelerate problem-solving and unlock new opportunities through Strategic Advisory and/or Projects.

This weekly newsletter highlights the top 3 stories from the past week in Food and Water Security and Net Zero transition, along with SOMA MATER’s analysis and perspective.

What are the main water-energy system challenges the Gulf region faces as it scales AI infrastructure?

How is Saudi Arabia strengthening food security while managing tightening water constraints?

How is Egypt using demand-management measures to reduce energy costs and protect supply amid higher oil prices?

Sustainably yours,

The SOMA team

AI Thirst: Data Centers, Water Tension

#FoodandWaterSecurity

The Gulf region’s push to scale AI infrastructure faces constraints. Without considering water efficiency and summer peak resilience, expansion risks overwhelming utility systems. Today, Gulf power and water networks are co-generation based, with electricity and desalinated water produced in the same plants. During summer spikes, when electricity demand rises sharply, this can limit the ability to produce additional water.

Technology helps, but in the long-term. Reverse osmosis (RO) improves desalination efficiency, but may take at least a generation before co-generation capacity is phased out. Recent weather events underscore why resilience matters: in the United Arab Emirates, one week of rainfall filled dams with roughly 72 million cubic metres of water, pushing storage to 83% of capacity.

A sole focus on energy is no longer enough. Regulators must adopt a holistic water-energy nexus approach. Data center growth must also be aligned with how water is produced and delivered. Across the region, the scale of current projects shows this momentum. Dubai announced completion of the first phase of its ‘Sewerage and Stormwater Network Development Project in Al Quoz Creative Zone’ (around $68 million so far). Saudi Arabia announced the completion of its water lines project, valued at $21.6 million. Kuwait also announced plans to build 6 underground reservoirs of up to 100 million imperial gallons each.

SOMA’s Perspective:

Unless regulators treat water and energy as one system, the next wave of digital infrastructure could create reliability risks. The near-term answer is not only more capacity, but smarter siting, cooling standards, and water-efficient desalination pathways, so the region can scale AI without turning resilience into an afterthought.

Berries, Eggs, and Beyond: Saudi Arabia’s Food Security Shift

#FoodandWaterSecurity

Saudi Arabia has reported rising self-sufficiency across crops and animal products. Data from the 2024 Food Security Statistics issued by the General Authority for Statistics (GASTAT) shows this performance. Crop self-sufficiency reached 121% for dates, 131% for dairy products, and 103% for table eggs, alongside 105% for eggplant and 100% for zucchini. Other items follow closely behind, including potatoes at 93%, tomatoes at 83%, onions at 72%, grapes at 65%, and mangoes at 55%.

Animal products show a similar picture. Shrimp has reached 149% self-sufficiency, poultry meat stands at 72%, red meat at 62%, and fish at 52%. The findings reflect the 4 dimensions of food security: availability, access, stability, and utilization. Progress in the Kingdom has stayed strong, but targeted investment is still needed to close remaining gaps.

Saudi’s Qassim Region is an example of this shift, growing quickly under Saudi Vision 2030. The region is increasingly known for black mulberries and berry cultivation, and projects are now scaling white, red, and blue varieties. In Unaizah, modern farms are reaching around 40 tons in annual yield, supported by closed-loop greenhouses, solar power, and precision climate control. Drip irrigation is helping farms cope with heat and water scarcity, while also reduced reliance on imports and supporting job creation.

SOMA’s Perspective:

This is a meaningful signal that the Kingdom is moving beyond headline investment and starting to translate policy into domestic supply, especially in staples. The harder work will be to sustain yields under tightening water constraints and building the cold-chain, inputs, and market infrastructure that makes surplus economically viable year-round.

Lights Out, Bills Down: Egypt’s Demand-Management Fix

#NetZeroTransition

The US-Iran conflict has pushed oil prices higher. Egypt is especially exposed because it relies heavily on imported fuel, leaving the economy vulnerable. In response, the government is leaning into demand-management as a first line of defense. It has focused on energy-saving measures that can be rolled out quickly.

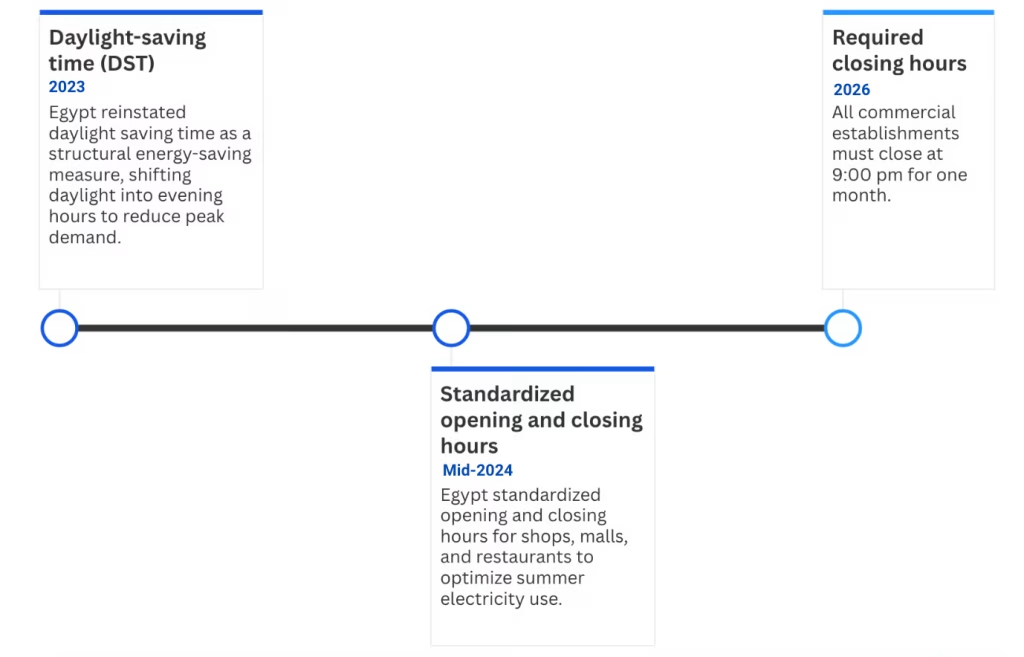

Time-based energy policies are at the center of this approach. In 2023, Egypt reinstated daylight-saving time, with cabinet estimates citing potential savings of up to 10%. In mid-2024, Egypt standardized opening and closing hours for shops, malls, and restaurants to reduce summer peak loads. This year, starting March 28th, commercial establishments, including restaurants, cafés, and shopping malls, were required to close at 9:00 pm for one month (Figure 1). Additional measures included switching off billboard lighting, reducing street lighting, and postponing diesel-intensive national projects.

Figure 1

These steps shift activity into homes, raising household electricity use. Yet even then, commercial spaces are up to 40% more energy-intensive per square meter. In a volatile fuel market, even a 5% reduction in electricity demand can translate into annual savings of hundreds of millions of dollars. On the fiscal side, Egypt has reduced energy subsidy allocations by around 20% in the draft FY 2026/2027 budget, setting EGP 120 billion versus roughly EGP 150 billion in FY 2025/2026. This rationalizes energy spending while protecting essential supply.

SOMA’s Perspective:

Egypt’s focus on demand management may be sensible in the short term, but it is not a structural fix: subsidy reform has been underway since 2014. The binding constraint is not awareness of what needs to be done, but execution capacity, from enforcing payment discipline to aligning incentives across a fast-growing population.

If you’d like to know more, contact us through:

Subscribe To Our Newsletter

Categories

- Events 3

- Intelligence Reports 2

- Newsletter 12

- Uncategorized 0

- Whitepapers 6